Cell And Gene Therapy CDMOs: On The Path To $75 Billion in Services?

By Louis Garguilo, Chief Editor, Outsourced Pharma

Cell and gene therapy (CGT) developers – and thus their service providers – have had their share of ups and downs. No need to rehash those right now.

But what might the uneven realities add up to in our development and manufacturing outsourcing sector?

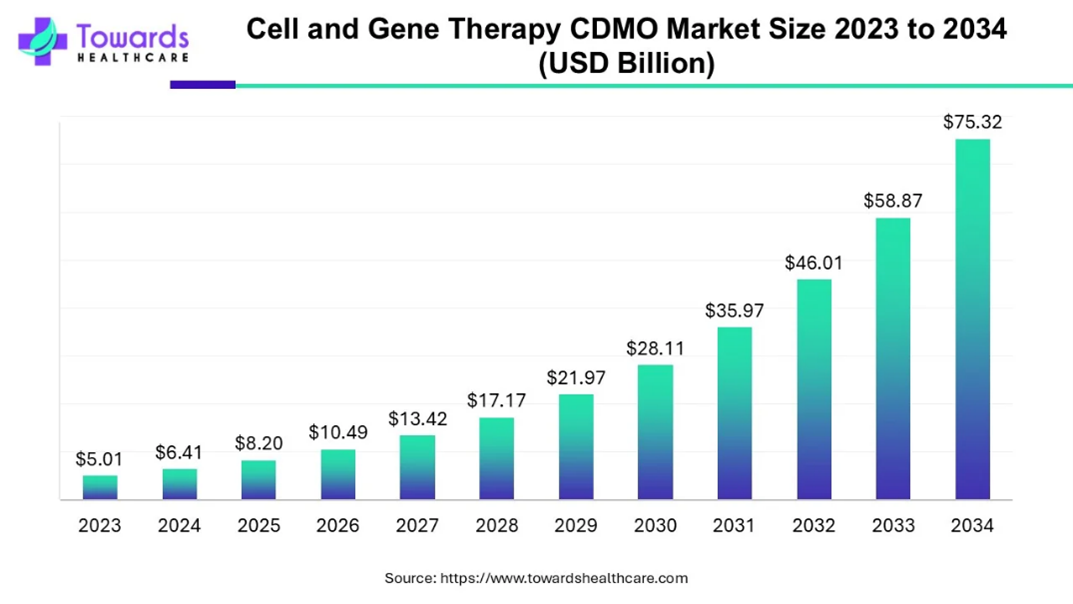

According to a Towards Healthcare report, in 2025 the global CGT CDMO market had already grown to $8.2 billion. The report projects a CAGR of 28% through the beginning of the 2030s. That would add up to a remarkable $75.32 billion by 2034.

Believable?

In spite of the well-publicized recent external capacity “glut,” sponsors (big and small) abandoning CGT research, the dissolving of some CDMO operations devoted to this area, the Towards Healthcare prognosis seems to offer a countering confidence in the science and manufacturing support needed for CGTs going forward.

I will, though, insert our habitual caveat: projecting a market so far into the future, while important directionally, can’t be taken as gospel. Some disproving examples from 2025:

- Pfizer discontinued the commercialization of Beqvez (fidanacogene elaparvovec), a recently FDA-approved AAV-based gene therapy for hemophilia B.

- Pfizer also stopped development of fordadistrogene movaparvovec for Duchenne muscular dystrophy (DMD) after it failed in a Phase 3 trial.

- Vertex discontinued all adeno-associated virus (AAV)-based gene therapy research. Biogen discontinued all gene therapy programs using AAV capsids, shifting resources away from early-stage gene therapies.

- Takeda ended its early-stage AAV work in 2023, and further exited the cell therapy space entirely by October 2025.

- Several CDMOs have recently reduced or closed their CGT operations due to market downturns and overcapacity, most notably AmplifyBio, which shut down in April.

- Other companies reducing their CGT footprint include Rentschler Biopharma (closing its UK site), Charles River Laboratories (divesting its CDMO business in 2026), and Thermo Fisher Scientific (closing its NJ site).

It's a thorny market where success and future hopes bloom precariously.

Not All About Those Numbers

Few areas of drug science depend more on CDMOs having to devise a profitable business model. Providers need to serve the idiosyncrasies of CGT development and manufacturing, and then flex as the industry and market endures its challenges.

These CDMO, says Sathe, “operate at the intersection of development, manufacturing, and regulatory execution. Advanced therapies can only succeed when manufacturing keeps pace with the science.”

In the past, CDMOs indeed rushed to establish innovative and compliant facilities, utilizing capital investment strategies, and training or hiring specialized knowledge workers.

Indeed, clinical trial activity continues apace. According to Sathe, regulatory data shows a trove of CGT studies actively progressing.

“Manufacturing readiness remains a critical factor in this trial continuity,” she says, and “flexibility is an essential element as programs evolve during clinical development.”

Interestingly, Sathe adds that personalized medicine now contributes noticeably to overall demand for these therapies requiring precise process and quality controls.

As the report puts it, “In personalized therapies, manufacturing precision directly affects patient outcomes.”

Precision … And Often Geography.

Sathe says geographic expansion plays an important role in Towards Healthcare’s projections of an escalating market for CGTs.

“While North America and Europe remain leading regions, Asia-Pacific markets are strengthening manufacturing infrastructure and regulatory alignment,” she says.

With most CGT therapies, the closer to the patient, the better the prognosis for effective therapy.

Notable are the medical centers, hospitals, and other healthcare venues that have reformed parts of their operations into veritable small-scaled CDMOs. The “supply chain” often benefits from reduced dependency on geographically removed manufacturing hubs.

At the same time, Sathe says a second “important shift within the market is the growing preference for end-to-end CDMO partnerships.”

“Many sponsors seek partners that can support development, scale-up, regulatory preparation, and commercial manufacturing within a single framework."

Cold storage, other logistical and highly tractable and technical networks and routes, integrated with traditional CDMO services, have and will need to further advance. Many therapies will continue to rely on temperature-sensitive materials and time-critical logistics.

Coordination across suppliers, transport, and storage is essential, and sponsors are buying into the mantra, when possible, that less distance and fewer handoffs often mean fewer delays.

The Manufacturing Complex

One point seems certain. Manufacturing cell and gene therapies remains complex. Despite standardization efforts and mounting experience, variability between programs is common and keeps manufactures on their toes.

We all know processes most often involve living cells, viral vectors, or genetic material that must be managed under a tight set of controlled conditions. Minor deviations can result in batch failure, and unlike some traditional pharmaceuticals, many products cannot be recovered once compromised.

According to the Towards Healthcare report, at the core of this overall complexity are several interlinked factors:

- Living biological materials behaving differently from batch to batch

- Highly sensitive processes where small deviations invalidate outcomes

- Limited tolerance for error due to direct patient impact

- Cold-chain dependency across every stage of production and delivery

- Tight scheduling windows tied to patient treatment timelines

- Limited margin for disruption in transport or storage

And thus … costs and pricing remains a central challenge.

As mentioned above, CDMOs for their part must invest in specialized facilities, advanced equipment, and skilled personnel ... then create (profitable) business models to flex as process and batch demand varies.

“Scaling production from research to commercial volumes requires sustained financial commitment,” Sathe says, and “regulatory requirements add further complexity.”

Global authorities enforce strict standards for quality, traceability, and patient safety; documentation and validation are as critical as process performance.

“I’ve seen my share of programs delayed not because of scientific limitations, but due to incomplete manufacturing records or insufficient validation data,” says Sathe.

Workforce availability and training remain a constraint struggle (despite what had been an over-capacity issue). CGT sponsors will tell you their experiences demonstrate that CDMOs prioritizing workforce development maintain higher consistency and operational stability.

Sathe says, “The cell and gene therapy CDMO market cannot be understood through market size alone. What our report reflects is how innovation, manufacturing discipline, and patient needs must converge with effective and evolving partnerships.”