Building CGT Manufacturing Capacity For The Next Commercial Era

By Lynette Nazabal and Riley Welch, Clarkston Consulting

As the life sciences industry moves beyond the disruption caused by the COVID-19 pandemic, manufacturers are facing a different set of pressures. Geopolitical uncertainty, tighter investment funding, and growing demand for flexible U.S.-based capacity are reshaping how companies plan for clinical development and build more resilient supply networks.

Cell and gene therapy (CGT) companies are feeling this pressure acutely. The global CGT pipeline continues to expand across a range of modalities, while the CGT manufacturing market is projected to grow at a 26.62% CAGR1 from 2025 to 2034. That growth is increasing demand for viral vectors and plasmids, along with reliable manufacturing facilities that can support these therapies at clinical and commercial scale.

For CGT companies, the challenge is not only securing manufacturing capacity for clinical development today but also building a path to commercial-scale production and sustained regulatory compliance. In response, contract development and manufacturing organizations (CDMOs) and contract manufacturing organizations (CMOs) are investing in capacity, automation, and standardized platform processes to support CGT developers more effectively. These investments are designed to improve throughput and accelerate release timelines while maintaining quality controls and allowing facilities to adapt as client pipelines evolve.

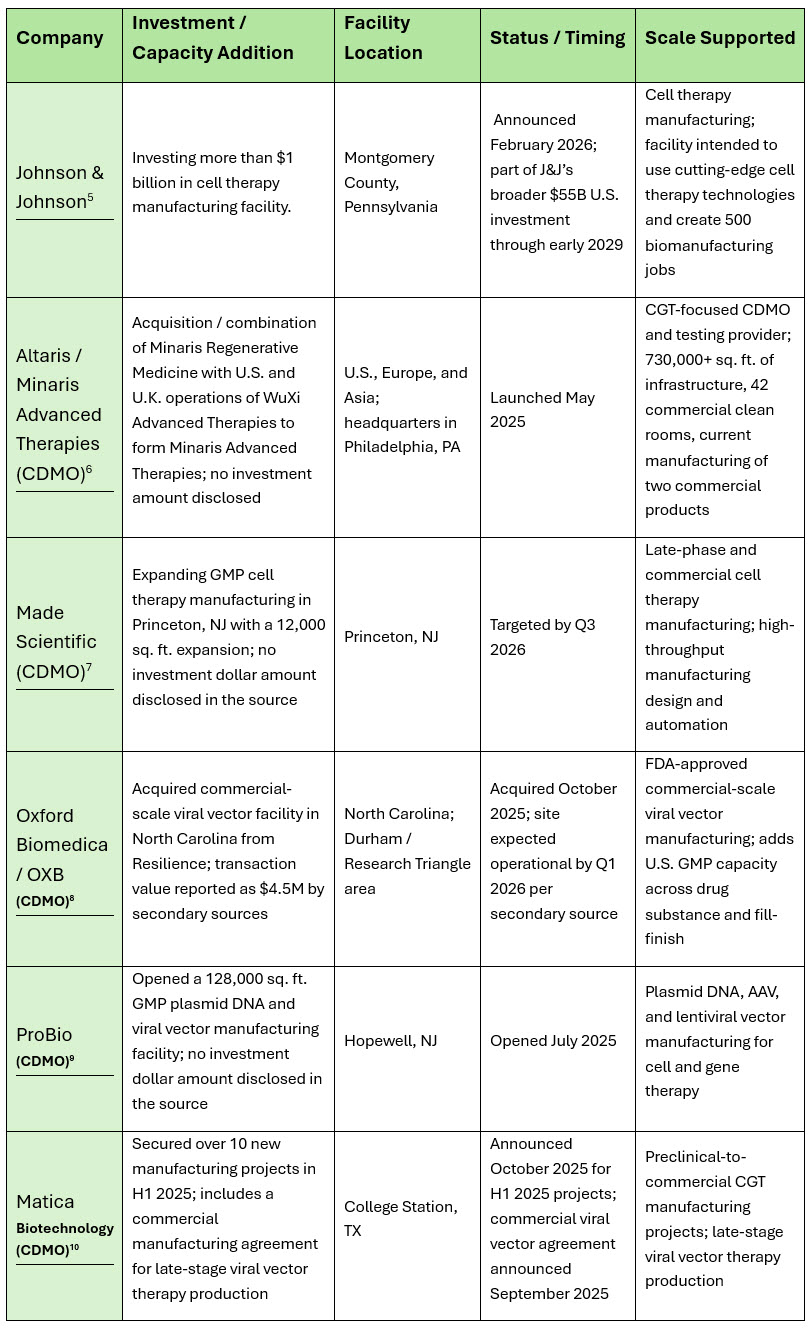

In this piece, we take a look at several recent investments — mostly by CDMOs and CMOs, though not solely — that are expanding manufacturing capacity to support the growing cell and gene therapy pipeline, associated technology and platform trends, and the impacts on CGT manufacturing from key M&As and geopolitical factors.

Investment Landscape

The CGT investment landscape has shifted significantly in recent years. After early-stage investment peaked in 2021, investors have become more selective, placing greater emphasis on later-stage opportunities with clearer paths to commercialization. Manufacturing has become a larger part of that investment picture, particularly as companies look for capabilities that can reduce execution risk.

Between 2021 and 2025, CGT deal activity declined by 66%,2 reflecting a broader pullback in venture capital and a reassessment of risk across the sector. As a result, capital allocation has moved away from early discovery programs and toward assets that can support long-term commercialization. This includes manufacturing infrastructure, process development capabilities, and platforms that can support scale-up.

This shift is particularly evident in the growing emphasis on integrated manufacturing. Investment is being directed toward facilities and equipment that can support the later stages of production. In response, manufacturers are building sites that bring together cell processing, vector production, and fill/finish capabilities to reduce the risk of bottlenecks.

CMOs and CDMOs are expanding flexible capacity and incorporating modular facility designs3 to accommodate evolving pipelines. Through site expansions, acquisitions, and new facility builds, they are positioning themselves to deliver scalable manufacturing solutions that can support CGT programs from clinical development through commercialization.

Collectively, the CGT industry is repositioning manufacturing assets to reduce risk4 and accelerate timelines for new therapeutic development. Investment is increasingly concentrated in scalable, U.S.-based systems designed to support long-term commercialization. In this environment, strong efficacy signals and robust CMC strategies have become critical priorities for companies seeking to attract and deploy capital.

Top CGT Manufacturing Investments

Capacity Constraints And Manufacturing Bottlenecks

As the CGT pipeline continues to expand and more therapies move toward commercialization, manufacturing bottlenecks are becoming more visible. While capacity expansion remains a major focus across the industry, differences in modality and regulatory readiness continue to shape how effectively available infrastructure can be deployed.

Historically, quality control has been one of the most significant bottlenecks in CGT manufacturing and remains a critical constraint today. Process complexity is also creating operational challenges across the manufacturing lifecycle, which can strain throughput and make it harder to maintain consistency as programs scale.

These dynamics point to a broader industry reality: capacity expansion alone does not eliminate bottlenecks. Constraints are shifting across the value chain, which is creating a need for more targeted investment in process efficiency and operational coordination.

Technology And Platform Trends

To address manufacturing complexity and scale, the CGT industry is increasingly investing in platform-based and technology-enabled approaches. These models aim to standardize key elements of the manufacturing process while preserving quality and accelerating timelines to commercialization.

Automated and closed manufacturing systems are transforming core CGT functions. By reducing reliance on manual operations, these systems can help lower error rates and reduce contamination risk. They also support scalability by enabling more consistent performance across manufacturing runs.

Digital and AI-enabled tools are also being adopted to improve production oversight and accelerate release timelines. AI-driven process control systems can monitor manufacturing in real time and detect deviations earlier. Process analytical technologies can strengthen in-process monitoring by generating more timely visibility into critical quality attributes. Together, these tools can improve yield while supporting regulatory compliance.11

CMOs and CDMOs are complementing these capabilities by packaging platform processes to shorten timelines and reduce CMC risk. For example, Catalent’s expanded UpTempo AAV platform incorporates clonal HEK293 cell lines and off-the-shelf plasmids, with the goal of reducing the time needed to manufacture clinical-quality drug product significantly.12 By providing standardized workflows, these platforms can reduce the time required to move from development into clinical production.

Beyond manufacturing, digital tools are also being applied to assess system readiness. Digital feasibility assessments are gaining traction as CGT expands into new therapeutic areas. As the industry moves from oncology into autoimmune indications, therapies may remain anchored13 in specialized centers that don’t always have the required infrastructure or IT integration to support broader patient access. Digital feasibility assessments can help identify risks related to product traceability and chain-of-identity integrity before those risks affect trial execution.

Collectively, these technologies and platform innovations are helping CGT companies improve consistency while preserving the flexibility needed to support an increasingly diverse therapeutic pipeline.

Impacts Of M&A And Financing On CGT Manufacturing

Mergers and acquisitions are playing an increasingly important role in the future of CGT. Rather than building every capability from the ground up, companies are acquiring platforms and facilities that can accelerate their entry into the market. Recent deal activity suggests that investors remain interested in advanced CGT modalities, particularly when assets have a clearer path to commercialization.

Recent M&A activity has been concentrated in areas such as CAR-T cell therapy and AAV-based gene therapy. Lilly’s acquisition of Adverum14 reflected continued interest in AAV-based gene therapy, anchored by Adverum’s Phase 3 intravitreal gene therapy candidate for wet age-related macular degeneration. Gilead’s acquisition of Arcellx15 deepened its investment in CAR-T therapy for multiple myeloma through anito-cel, an investigational BCMA-directed CAR-T therapy.

This large biopharma M&A activity highlights the strategic appeal of platform acquisitions16 as companies compete for leadership in emerging CGT modalities. It also shows how later-stage assets can attract capital even in a more selective funding environment.

Consolidation is also happening among CMOs and CDMOs. GI Partners’ acquisition of Charles River Laboratories’ CDMO and Cell Solutions businesses,17 followed by the formation of Rose BioSolutions, reflects a broader push toward specialized advanced therapy manufacturing platforms. Rose BioSolutions brings together plasmid DNA, viral vector, cell therapy manufacturing, and cellular starting material capabilities across facilities in the U.S. and U.K., positioning it as a dedicated CGT manufacturing partner.

Across the industry, M&A activity continues to reinforce that scale and technical differentiation are becoming essential to compete in an increasingly complex market.

Impacts Of Regional Strategy and Policy On CGT Manufacturing

Geography and policy are playing an increasingly influential role in shaping CGT manufacturing strategy. North America accounted for just over half of the global CGT manufacturing market in 2025,18 reflecting the region’s strong base of manufacturing capacity and development activity. Ongoing uncertainty around tariffs and global trade is reinforcing interest in domestic manufacturing as companies look to reduce supply chain exposure.

On the regulatory front, FDA has outlined19 a more flexible approach to CMC oversight for CGTs. The agency states that manufacturers are not expected to comply with 21 CFR Part 211 before investigational products are manufactured for Phase 2 or Phase 3 trials. This flexibility is intended to help expedite product development while maintaining expectations for safety and quality.

Policy uncertainty is also introducing new strategic considerations. The Trump administration’s Section 232 tariff framework imposes a baseline tariff20 of 100% on certain patented pharmaceuticals and associated ingredients, while also establishing reduced rates and exemptions for some imports. This type of policy environment21 could increase pressure on companies that rely heavily on overseas manufacturing, particularly as they evaluate commercial margins and launch sequencing.

Most Favored Nation22 pricing policies may also influence commercialization planning. If lower ex-U.S. prices affect U.S. pricing benchmarks, companies may need to reassess launch timing and global trial sequencing. As a result, manufacturing strategy is becoming more closely tied to market access planning.

Overall, these regional and policy dynamics are reinforcing a broader shift toward localized manufacturing networks designed to support more resilient CGT commercialization.

Industry Outlook And Recommendations

Thoughtful analysis of your commercial model, coupled with digital strategy and company goals, should inform investment and expansion of CGT manufacturing footprint. As companies start to understand their patient population, their potential growth, and what they’re going to market with, they’re in a stronger position to decide whether to buy or lease versus leveraging an already-established CDMO.

For many organizations, outsourcing can provide a faster path to manufacturing readiness, especially when speed matters more than ownership. For others, greater control over manufacturing may be essential to protect product quality and support long-term supply resilience.

The right answer will vary by company and by asset. What matters most is making deliberate choices early, before manufacturing becomes the constraint that slows everything else down.

References

- Precedence Research. (2025, December 4). AI-Powered Cell and Gene Therapy Manufacturing Market Outlook 2034 Scaling Advanced Therapies with Digital Innovation. BioSpace. https://www.biospace.com/press-releases/ai-powered-cell-and-gene-therapy-manufacturing-market-outlook-2034-scaling-advanced-therapies-with-digital-innovation

- Barrie, R. (2025, December 10). Cell and Gene Therapy Investment Strategy Pivots as Funding Dries Up. Pharmaceutical Technology. https://www.pharmaceutical-technology.com/news/cell-and-gene-therapy-investment-strategy-pivots-as-funding-dries-up/

- Made Scientific. (2025, May 29). Made Scientific Powers Late-Phase and Commercial Cell Therapy Manufacturing with 12,000 sq. ft. Expansion in Princeton, NJ GMP Facility. Made Scientific. https://madescientific.com/news/made-scientific-powers-late-phase-and-commercial-cell-therapy-manufacturing-with-12000-sq.-ft.-expansion-in-princeton-nj-gmp-facility

- OXB. (2025, October 7). OXB Expands US Footprint with Acquisition of Commercial-Scale Viral Vector Facility in North Carolina. OXB. https://oxb.com/news/oxb-expands-us-footprint-with-acquisition-of-commercial-scale-viral-vector-facility-in-north-carolina/

- Johnson & Johnson. (2026, February 18). Johnson & Johnson Expands U.S. Footprint with More Than $1 Billion Investment in Next Generation Cell Therapy Manufacturing Facility in Pennsylvania. Johnson & Johnson. https://www.jnj.com/media-center/press-releases/johnson-johnson-expands-u-s-footprint-with-more-than-1-billion-investment-in-next-generation-cell-therapy-manufacturing-facility-in-pennsylvania

- Minaris Marketing. (2025, May 7). Minaris Advanced Therapies Launch. Minaris. https://minaris.com/minaris-advanced-therapies-launch/

- Made Scientific. (2025, May 29). Made Scientific Powers Late-Phase and Commercial Cell Therapy Manufacturing with 12,000 sq. ft. Expansion in Princeton, NJ GMP Facility. Made Scientific. https://madescientific.com/news/made-scientific-powers-late-phase-and-commercial-cell-therapy-manufacturing-with-12000-sq.-ft.-expansion-in-princeton-nj-gmp-facility

- OXB. (2025, October 7). OXB Expands US Footprint with Acquisition of Commercial-Scale Viral Vector Facility in North Carolina. OXB. https://oxb.com/news/oxb-expands-us-footprint-with-acquisition-of-commercial-scale-viral-vector-facility-in-north-carolina/

- ProBio. (2025, June 27). ProBio Opens Flagship U.S. Plasmid & Viral Vector Manufacturing Facility in Hopewell, New Jersey to Advance Cell and Gene Therapy. ProBio. https://www.probiocdmo.com/probio-opens-new-facility-in-hopewell.html

- Matica Biotechnology, Inc. (2025, October 6). Matica Biotechnology Emerges as the Go-To CDMO for Cell & Gene Therapy. Matica Biotechnology. https://www.maticabio.com/news-events/newsroom/matica-biotechnology-emerges-as-the-go-to-cdmo-for-cell-gene-therapy/

- AGC Biologics. (2025, October 29). Trends Shaping the Future of Cell and Gene Therapy Manufacturing. AGC Biologics. https://www.agcbio.com/biopharma-blog/trends-shaping-the-future-of-cell-and-gene-therapy-manufacturing

- Catalent, Inc. (2023, March 9). Catalent Expands UpTempoSM AAV Platform to Accelerate Development of Gene Therapies. Outsourced Pharma. https://www.outsourcedpharma.com/doc/catalent-expands-uptempo-sm-aav-platform-to-accelerate-development-of-gene-therapies-0001

- Ndugga-Kabuye, K. (2026, January 6). De-Risking the Future of CGT: Emerging Trends Redefining Execution, Evidence, and Asset Value. Premier Research. https://premier-research.com/perspectives/de-risking-the-future-of-cgt-emerging-trends-redefining-execution-evidence-and-asset-value/

- Waldron, J. (2025, October 24). Eli Lilly Buys Cash-Strapped Adverum for Its Phase 3-Stage Eye Disease Gene Therapy. Fierce Biotech. https://www.fiercebiotech.com/biotech/lillys-buys-cash-strapped-adverum-its-phase-3-stage-eye-disease-gene-therapy

- Giboney, M. (2026, February 26). Cell Therapy Weekly: Acquisition to Advance CAR-T Therapy for Multiple Myeloma. RegMedNet. https://www.regmednet.com/cell-therapy-weekly-acquisition-to-advance-car-t-therapy-for-multiple-myeloma/

- ISCT Business Development & Finance Committee. (2025, December 8). Tracking Capital in CGT: Emerging Trends in M&A and Series Funding. ISCT Telegraft Hub. https://www.isctglobal.org/telegrafthub/blogs/francheska-juliano/2025/12/08/tracking-capital-in-cgt-emerging-trends-in-ma-and

- GI Partners. (2026, May 7). GI Partners Completes Acquisition of the CDMO and Cell Solutions Businesses from Charles River Laboratories and Forms Rose BioSolutions. PR Newswire. https://www.prnewswire.com/news-releases/gi-partners-completes-acquisition-of-the-cdmo-and-cell-solutions-businesses-from-charles-river-laboratories-and-forms-rose-biosolutions-302765625.html

- Debashree B. (2026, March 16). Cell and Gene Therapy Market Size, Share & Trends Analysis Report. Straits Research. https://straitsresearch.com/report/cell-and-gene-therapy-market

- U.S. Food and Drug Administration. (2026, January 11). Flexible Requirements for Cell and Gene Therapies to Advance Innovation. FDA. https://www.fda.gov/vaccines-blood-biologics/cellular-gene-therapy-products/flexible-requirements-cell-and-gene-therapies-advance-innovation

- Ilancheran, M. (2026, April 15). U.S. Pharma Tariffs and MFN Become Law After April 2 Update. Clinical Leader. https://www.clinicalleader.com/doc/u-s-pharma-tariffs-and-mfn-become-law-after-april-update-0001

- Ndugga-Kabuye, K. (2026, January 6). De-Risking the Future of CGT: Emerging Trends Redefining Execution, Evidence, and Asset Value. Premier Research. https://premier-research.com/perspectives/de-risking-the-future-of-cgt-emerging-trends-redefining-execution-evidence-and-asset-value/

- Birbeck, I. & Firestein, J. (2026, February 6). Unpacking the Potential Implications of the TrumpRx-Pfizer Deal. Clarkston Consulting. https://clarkstonconsulting.com/insights/implications-of-the-trumprx-pfizer-deal/

About the Authors

Lynette Nazabal is an associate partner at Clarkston and leads the firm’s pharmaceutical, biotech, contract manufacturing, and contract research organization work. In this role, she provides oversight and guidance for services and solutions serving these industries. Lynette has nearly 20 years of experience across quality systems, manufacturing, commercialization, laboratory operations, validation, regulatory compliance, and technology. She also has deep expertise in manufacturing execution systems and has partnered with infrastructure and information security teams to deliver cloud-based solutions for life sciences.

Lynette Nazabal is an associate partner at Clarkston and leads the firm’s pharmaceutical, biotech, contract manufacturing, and contract research organization work. In this role, she provides oversight and guidance for services and solutions serving these industries. Lynette has nearly 20 years of experience across quality systems, manufacturing, commercialization, laboratory operations, validation, regulatory compliance, and technology. She also has deep expertise in manufacturing execution systems and has partnered with infrastructure and information security teams to deliver cloud-based solutions for life sciences.

Riley Welch is a consultant at Clarkston with experience across the life sciences and consumer products industries. At Clarkston, she has supported LIMS implementation, training, and validation, as well as SOP review and development, supply chain assessment, and strategic business transformation work. Before joining the firm, Riley worked in pharmaceutical quality operations and conducted independent life sciences research. She thrives in dynamic, team-driven environments and brings a client service mindset to complex challenges. Riley holds a B.S. in Biology with a minor in Neuroscience from UNC-Chapel Hill.

Riley Welch is a consultant at Clarkston with experience across the life sciences and consumer products industries. At Clarkston, she has supported LIMS implementation, training, and validation, as well as SOP review and development, supply chain assessment, and strategic business transformation work. Before joining the firm, Riley worked in pharmaceutical quality operations and conducted independent life sciences research. She thrives in dynamic, team-driven environments and brings a client service mindset to complex challenges. Riley holds a B.S. in Biology with a minor in Neuroscience from UNC-Chapel Hill.